Financial independence is a key goal for many women, but so few achieve it. What is one of the main factors influencing success or failure? Coming up with an action plan for your specific financial situation and making a commitment to stick with it. Read on for actionable advice to kickstart your own journey towards financial independence.

1. Determine your why. You need a reason that’s bigger than your fear of change.

Starting with a clear picture of where you are now and what you need to do to get where you want to go is key to meeting your financial goals. Create a vision for your perfect life. Scribble all of your wishes, dreams and wants out on paper and put together a vision board. Making your vision feel real will allow you to begin to believe it’s attainable. Self-reflection is incredibly important – you want your vision to be uniquely you. And you need to know what you want to truly be motivated to stay the course.

It’s time to figure out the following things:

- What does financial independence mean to you? Don’t follow someone else’s definition—personalization is key to buying in to your dreams.

- A clear picture of your current financial situation. Where are you on your journey? Are you starting in debt? Or have you already been saving for years?

- A realistic idea of what you may need to give up to achieve your gals

- An assessment of the obstacles in your path

- A set of goals that fit your unique financial situation

For me, financial independence is the point at which you no longer need to work for a living. Doesn’t mean I’ll stop working, but I won’t need a paycheck. I’ll be free from having to work for a living.

Far away there in the sunshine are my highest aspirations. I may not reach them, but I can look up and see their beauty, believe in them, and try to follow where they lead.

– Louisa May Alcott

2. Break your big financial independence goal down into mini goals, or steps

There are a number of key areas you should set goals in if you want to achieve financial independence:

- Increasing your income

- Controlling your spending

- Paying off debt

- Improving your understanding of how you tend to save and how to motivate yourself to achieve even more

- Determining your investment objectives and timelines

- Clearly defining your long-term financial goals

- Protecting your assets and increasing your security (Do you have enough insurance? Are your finances ready to handle a health scare?)

- Creating a legacy plan (Do you want your wealth to transfer to your heirs? Would you like to set up a donor advised fund for charitable giving?)

- Setting life goals (What do you want your life to look like when you reach financial independence? What steps can you take along the way?

Realize that small, steady steps over time make a big difference. Take the time to celebrate all of these wins. By breaking your big goal down into pieces you’ll make it attainable.

With a goal like financial independence, slow and steady wins the race. You don’t need to go from 0 to 60 overnight. Sure, people who make extreme changes grab the headlines, but as with anything, those are hard to maintain. Its less sexy to take the slow and steady path, but you’re more likely to make it to your end goal. Do everything you can to automate your savings and make the financial independence journey easier on yourself. If you’re putting your savings out of mind and out of sight the majority of the time, you’ll be less tempted to spend them frivolously.

By recording your dreams and goals on paper, you set in motion the process of becoming the person you most want to be. Put your future in good hands—your own.

– Mark Victor Hansen

3. Learn that income is not wealth

It’s important not to confuse high income with wealth. While high income may help you reach your financial goals faster, anyone can take steps to improve their financial position regardless of their income. And there are many examples of people with regular incomes achieving financial independence. it just may take longer than the stories of tech bros living out of a van and saving 90% of their income!

It’s easier to amass assets if you have more money coming in every month, but the only secret to building wealth and increasing your own net worth is to spend less than you make.

What is wealth? The part of your net worth (assets minus liabilities) that generates capital gains, income and dividends without your labor. Your level of wealth tells you how long you could keep up your purchasing patterns if you stopped working right now. That’s why you’ll occasionally hear stories of big stars who suddenly file for bankruptcy when they hit a lull in their career. They may have income levels unattainable for the average person, but if their expenses are higher than their income, they can quickly run into trouble.

What is the value of wealth? Maintaining your lifestyle, even if you are unable to continue working. Wealth can’t fire you. You can lose your wealth through mismanagement, but it’s easier to lose a job than to wipe out a well constructed asset portfolio.

4. If you have a partner, make sure that you’re on the same page

No matter how successful you and your spouse are, if you’re not both on board you’ll make slow progress towards your financial independence goal. It’s important that you work together to proactively set goals for your life and implement a plan to achieve them. You’ll have the support to take risks. And you’ll reach your goals faster if you’re working together. When you have the same clear goals in mind it’s so much easier to avoid the urge to keep up with the Joneses.

5. Commit to living below your means

It’s pretty simple. Your savings need to outweigh your expenses for you to have any hope of success in reaching financial independence.

Keeping your big goal in mind will help you resist when faced with the temptation to splurge. Practicing delayed gratification and really taking the time to think through each purchase will help you become conscious of your own impulse buying triggers.

Limit your exposure to people who live beyond their means. If your friend circle all lives for the moment and keeping up with them knocks you off track, be creative with affordable ways to get together and say no to regular splashy nights out. Minimize the temptation to participate.

6. Cut your costs

It’s totally normal to dread cutting costs. But if you want to achieve big goals like financial independence, it’s important to scrutinize your spending and be conscious of the impact of your purchases. Keep your big goals in mind.

What are your fixed and variable expenses? Fixed expenses are harder to change and you cannot avoid them without seriously affecting your life (ex: rent/mortgage, electricity, food, transportation, insurance, loan payments). Variable expenses are easier to tackle quickly, because they’re completely discretionary (ex: cable, coffee, gifts, eating out, miscellaneous spending money, etc.) Work on eliminating or cutting back on variable expenses, and reducing fixed expenses.

It’s a cliché, but the financial impact of buying coffee on the way to work every day is real. Say you purchased 1 cup every workday (M-F) for $4 per cup. If Instead you put $4 per day, or $20 per week, into investments with 7% annual rate of return, that coffee money would grow to $15k+ within 10 years.

And if you did this every day from ages 20 – 65? That coffee money would grow to more than $300,000! Where can you get creative with your budget? When you look at the big picture, every $20 invested per week is totally worth it.

Here are some expenses to start with:

- Cut cable. Try Netflix, Hulu, HBOGo, etc. There are a lot of options these days and so many better ways to spend your time

- Try a challenge to lower your bills. Do you know what you’re spending on water? Electricity? Try adding one easy hack in a week and see how low you can go

- Learn to cook & add a meatless meal day to your week. Follow me on Pinterest for a collection of affordable recipe ideas

- Take a few hours to check your insurance costs and see if you can get a better deal

- Decrease your cell phone bill. Look into Republic Wireless. Tell your kids they need to pay for their own phones.

Ready to tackle the bigger expense categories?

- Find ways to cut your transportation expenses

- Cars are a huge expense. Could you drive a little less by biking to work once a week? Batching your errands?

- Can you increase your gas mileage by following the speed limit?

- Could you carpool occasionally? Or take public transportation?

- Explore whether house hacking is a viable option for you

- Could you get a roommate and split the bills?

- Could you move to a smaller place with income generating potential? (i.e. a duplex)

- How much could you earn by renting out your home occasionally during tourist season?

- Cut back on your grocery spending. Groceries are often one of the biggest expense categories families have. But eating well on the cheap is possible! The keys to cutting your grocery expense?

- Set a budget

- Make a list and don’t deviate, unless you find a good deal on a staple

- Eat before shopping so you’re less likely to cave and grab pricey prepared snacks

If it feels overwhelming, try exploring one category per week. Slow and stead steps in the direction of your goals is the key to success. Brainstorm a list of cost cutting ideas you can tackle when you have a few free moments.

7. Stop trying to impress others with things.

Keeping up with the Joneses will slow your path to financial independence. Keep your big goals in mind when deciding whether to replace your car (waiting another year each time you’re ready to upgrade can make a big difference over a lifetime), move to a bigger house, or spend on splashy vacations or wardrobes.

Delaying gratification can help speed up your journey to financial independence. Even better, you’ll frequently find that by delaying purchases the impulse to buy fades, the price of the item drops, or you realize you can do without.

8. Increasing your income can be a huge boost on your path to financial independence

By cutting back expenses and consciously minimizing lifestyle creep you’re essentially front loading sacrifice so that you have freedom and flexibility sooner than the average person. It may feel difficult now, but once you achieve your goals you’ll truly be free while many of the people you may have envied along the way are still stuck with credit card debt, car loans, large mortgages, etc.

While you may ultimately want to retire early, committing to keeping your career or business moving forward will help you immensely on your journey. By increase your skills, you make yourself even more valuable in the work force. And the more your salary increases and you hold your expenses steady, the greater your contributions to savings and debt repayment and the faster you will achieve your goal.

Do you know your savings rate?

Start by taking your after tax income and adding on the amount contributed to your 401k, or other pre-tax retirement accounts. If this is $100,000 and you save $20,000 for retirement (401k contributions + other retirement savings), you’re saving 20% for retirement.

($20,000/$100,000) x 100% = 20% savings rate

If you were starting from zero today and expected to maintain the same $80k spending in retirement, it would take approximately 30 years and 8 months of saving $20k per year to save up $2 million and reach your goal.

If you were to save only 10% of your income, it would take you 41 years to reach your goal.

Interested in figuring out how soon you can retire using different scenarios and savings rates? Check out the Networthify retirement calculator.

9. Avoid being penny wise but pound foolish

It’s tempting to save a few dollars here and there when buy small items. But when you have to drive to multiple stores and spend extra time to get these savings, or when you’re buying things you don’t need because they’re a good deal, you may not be making progress toward your goals. Know the value of your time. If you could earn more through a side hustle or overtime work, it may make sense to pay someone to clean your house or deliver your groceries. Outsourcing low value tasks can free up time for earning more money or taking other steps to advance your goals.

10. Don’t put off saving

It’s critical that you begin saving now. Too many people tell themselves “I’ll start saving when…” and it never happens. There’s always another reason to delay. No matter what you make, begin setting aside a little bit every paycheck.

Compound interest is your friend and it takes time. I’m so grateful I listened to the advice to always save 10% of my income in a 401k when graduating college. Early on those annual contributions didn’t amount to much, but it’s added up over the years and those early dollars are worth so much more today through the magic of compounding.

Don’t allow yourself to make excuses. Set your savings goals and take small steps every day to achieve success.

That said, you must have surplus funds to invest. It’s why decreasing your expenses and increasing your income are so important. Achieving financial independence and building wealth are slow processes that take time. The more you can increase your available dollars for investing, the quicker you’ll make progress towards your goal. Through compounding the interest, dividends and capital gains the dollars you invest will grow over time.

Interested in learning more?

11. Consider geographic arbitrage to speed up your path to financial independence

Many people feel stuck on their current path. But you have more flexibility than you think. Especially if you’re young and unencumbered by a spouse and children—could you relocate to bring your FI date even closer? Perhaps your job in a high cost of living city will let you work remotely. Perhaps you have an online business where you could spend part of the year living someplace where your income will go much further. Spend a few months abroad in a country like Thailand or Mexico and you can experience a new culture while turbocharging your investments. Could you teach English abroad? Some programs even provide with housing!

12. Realize millionaires may not be who you think

According to Thomas J. Stanley, author of The Millionaire Next Door:

- The grades you earn in school are not correlated with wealth and economic success, except in the medical and legal professions

- The majority of millionaires wear jeans – not a suit

- Most millionaires own their own businesses

It’s a myth that good students go further in life. Schools only measure a limited range of the types of intelligence. If you’ve been allowing your past to hold you back, or expecting that your good grades will guarantee you an easy path forward, let go of those ideas now. Your life is what you make of it.

An average person with average talents and ambition and average education, can outstrip the most brilliant genius in our society, if that person has clear, focused goals.

– Mary Kay Ash

13. Protect yourself with an emergency fund

Don’t let small financial setbacks derail your journey. Create a safety net by having a small emergency fund. Are you paying back debt? It’s fine to keep your emergency fund small early on while you tackle other goals. Eventually you should build it up to cover a few months of expenses, but if you have credit card or student loan debt it may make sense to keep a small fund on hand for emergencies but dedicate the bulk of your free cash flow to speeding up your debt repayment.

Life is full of surprises and an emergency fund gives you flexibility.

Interested in learning more?

14. Begin investing and determine your retirement plan

Most people can figure out a simple investing strategy for themselves, but it can help to use an adviser if it increases your comfort level. Just make sure you select someone who has a fiduciary responsibility to make suggestions that are in your best interest.

Where should you start when it comes to investing? First, determine whether you’re saving for short or long term goals. Second, choose investments that match your risk profile and time horizon. And finally, funnel any extra or unexpected income into your investments. It’s that simple!

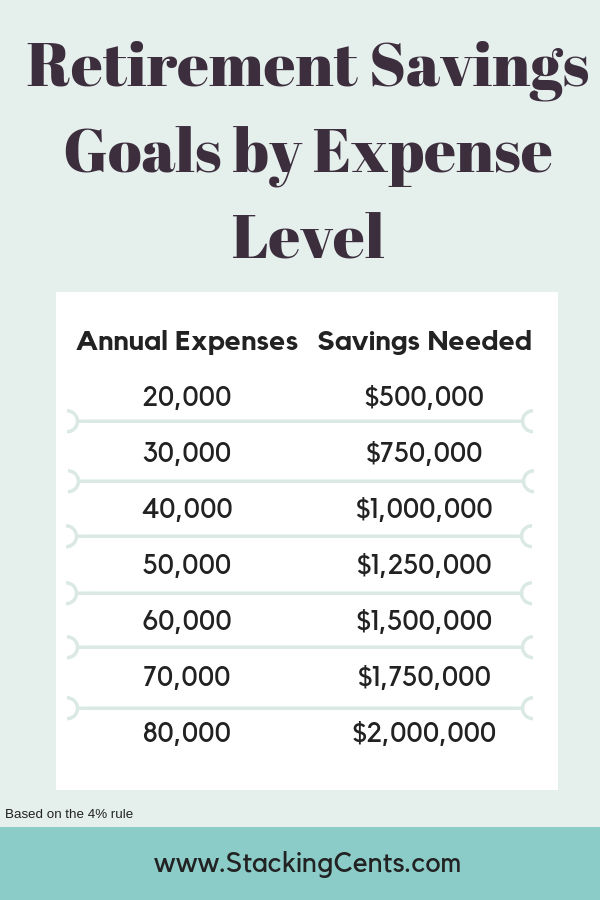

A rough rule of thumb for building a retirement portfolio is that you need to invest 25 times your annual spending. If you spend $20k, that’s $500k. If you spend $40k annually, that’s $1 million. This aligns with the safe withdrawal rate, which many people refer to as the 4% rule. It comes from the Trinity Study, a nickname for a paper on choosing a sustainable withdrawal rate. Essentially the safe withdrawal rate is the highest sustainable withdrawal rate in the worst-case scenario for rolling periods of historical data that they found. The big caveat – there’s no guarantee that the future will be like the past.

The safe withdrawal rate is the maximum rate at which you can withdraw or spend your retirement savings, so that they don’t run out in your lifetime. These studies assume that your savings appreciate 7% per year on average and that inflation take 3% of that on average, leaving you with 4% you can reliably spend. All of these simulations are theoretical and are complicated by things like high inflationary periods and sequence of returns risk (i.e. your likelihood of success increases if your investments do well during your first few years of your retirement). The values of stocks and real estate go up and down every year and so does the rate of inflation. These calculations all depend on long term averages.

Having some flexibility in your budget can protect you further from risk. Could you cut expenses during a downturn? Or earn a little more in lean years, so you don’t need to withdraw as much? Do you have enough insurance to minimize the variability of some large expenses?

15. Don’t try to time the market

If the pros can’t beat it, the likelihood you will is incredibly low. Focus on making slow and steady investments over time and you’ll essentially be dollar cost averaging your way into the market. The one exception? If all signs indicate the market is really hot, maybe increase your cash cushion so you can plow that money into the market when the inevitable downturn eventually comes. But know yourself first. If you’re going to have a hard time making a big investment when the market drops, you are likely better off better off putting that same money in slowly now.

Most people who lose money in the stock market are trying to time the market by buying low and selling high. It sounds obvious, but with all the experts trying to do it, very few succeed. The market is nearly impossible to predict, and mutual fund firms will charge you high fees to attempt it. Our solution? Just ignore it and invest in index funds. Expense ratios are low if you aren’t trying to pay someone to pick winners and losers.

And keep your big goals in mind and avoid the urge to panic. If you’re checking your numbers and freaking out every time the market drops, you’re doing yourself a disservice. Stay the course. The market has always come back eventually.

16. Diversify your investments

In general, it’s a good strategy to focus on low fee options (i.e. index funds) but contrary to some of the voices in the financial independence space, it’s okay if you don’t want all your eggs in one basket. The equity markets have become less diverse over time and we really don’t know what the long-term implications of that are. Plenty of stocks appear to be overvalued and there is a winner-takes-all component to tech lately. Rather than follow the herd, choose investments that fit your risk profile.

If you know you’ll be bothered by high volatility, explore keeping some of your investments in bonds, cash or real estate. Everyone has their own journey and risk tolerance – it’s okay to customize your investment portfolio to meet your needs and best suit your skill set.

17. Diversify your income sources

The more streams of income you have, the lower your risk. If you’re relying solely on a high paying job, what happens if you’re laid off? If the idea keeps you up at night, it may be time to diversify your income sources.

Could you start up a side hustle to generate additional cash? Have you explored investing in real estate? Or investing in stocks that generate dividends? Is your spouse employed? Knowing how you would meet your basic expenses in the face of an unexpected layoff or bad month will increase your peace of mind.

And diversification is important for the self-employed too. If you’re a wedding photographer, perhaps you could take family photos during the off season. And if you’re a blogger relying on advertising income, perhaps you could explore affiliate sales. Think creatively about how you can minimize risk in your own life through diversification.

18. Budget your time wisely

At first you may balk at the idea of taking on a second job. You work hard and need your leisure time. Consider tracking your time for a week to see where it goes. Americans watch an average of 5 hrs of TV a day, which adds up to 35 hours per week—nearly another full time job! Can you reclaim a portion of that time and spend it on something that will speed up your journey to financial independence? Perhaps you could babysit through Care.com, dog walk through Rover.com (bonus points for the extra exercise!), or drive for Uber.

19. Consider working with a tax professional to optimize your taxes

We haven’t taken this step yet and I’m sure we’ve left money on the table by not optimizing.

Taxes matter a lot. In general, people with no wealth and high income generate a lot of taxable income. A person who is financially independent and largely living off unrealized gains in the form of real estate appreciation, profits made through tax-advantaged or tax-free accounts, and capital gains on investments that are taxed at a lower rate than the tax on earnings from employment will pay a lot less in taxes.

For example, if you’re a professor earning $250k per year it’s likely you’ll be taxed heavily, paying approximately $95k in taxes for a net income of $155k. Yet if you are earning the same amount within a pension plan, 401k, or IRA, you could owe little to nothing in taxes as long as you worked with a professional to learn how to time your withdrawals in a tax efficient manner.

At a minimum, make sure you’re investing in any tax deferred retirement accounts through your workplace that offer an employer match.

20. Get out of debt

Debt costs you money every month. It’s difficult to reach your financial independence goals if your progress is being held back by debt. We should know—we’re still working our way through six figures of student loans! I cringe looking back at all the time we’ve lost where the money we’re spending on debt repayments could have been compounding in our savings. While investing in your education is important, its not a guaranteed path to financial freedom and I wish I’d had a better understanding of the risks of graduating into a recession.

There are different types of debt and some are better than others. But in general, you should pay off high interest rate debt first. It’s also important to tackle debt that couldn’t be discharged in bankruptcy in a worst case scenario situation, such as student loans. It helps to tackle debt strategically and determine a plan for which order you want to tackle your particular debts in.

Once you’ve begun cutting back on expenses, you may see loan payments making up a larger part of your monthly expenses. Once they’re gone, you’ll really be able to ramp up your savings if you choose! When we started our monthly minimums on student loans were over $2k per month. It was insane and every time we pay one off and bring down our monthly minimum, it’s like a huge weight has been lifted.

Financially it often makes the most sense to target your highest interest rate loans first. But, psychologically it can help to see progress by paying off your loans with the lowest balances first. This increases your free cash flow. And the best part? The rate of debt payoff accelerates over time, as more money goes towards the principal balance than the interest, making progress easier.

Consider taking on extra work opportunities to pay down your debt faster and put any windfalls (gifts, bonuses, etc.) towards your debt. Think of windfalls as for buying freedom, not a spa day or fancy shoes to maintain excitement.

21. Avoid lifestyle inflation

Its so tempting to spend more as you earn more, but if you can avoid inflating your lifestyle you can expedite your journey to financial independence. If your needs are lower and your earnings are higher you’ll fast track your path to success.

Make sure you’re not giving up what you want most for what you want now.

22. Match your spending to your priorities

As Paula Pant says, you can have anything but not everything. What truly matters to you? To your family? Going overboard with saving can make you miserable and its likely to be a long journey to financial independence. While you should limit lifestyle inflation, it’s important to seek balance with conscious spending on things that make your life better. Do you want someone else to clean your house? Or do you value spending more for local and organic foods? Aligning your spending with your values and spending on experiences over things have both been shown to have positive effects on well being.

23. Protect yourself with insurance

Do you have enough insurance coverage? As you begin to build wealth, it’s important to ensure your progress isn’t derailed by an unexpected event. Spending on quality health insurance and to make sure you have enough homeowners, life, and disability insurance to cover you and your family in a worst case scenario situation is an important piece of setting yourself up for financial independence.

24. Never having to work again is very different from never working again

Perhaps you want to stay home with children while your spouse continues to work. Perhaps you’ll continue working in some capacity and generate enough money to cover your discretionary expenses. It’s okay if your path is different from the save up $1 million+ and never work again crowd. Even a small part time job can make a huge difference in how much you need to draw down your investments or whether you can continue to let them grow.

True wealth gives you control over your time. Wealth lets you choose how to spend your days, whether you have a passion for your career and choose to continue or not.

I recommend the following bloggers take on the topic:

- Mr. Money Mustache: First Retire, Then Get Rich

- Mad Fientist: Shortest Path to Financial Independence

25. Regularly check in on your goals

It’s important to schedule annual and monthly touch bases to check in on your goals and adjust your path as needed. What’s changed? Are your goals the same? Are you on track? Do you have additional income you can now utilize? Make time to make adjustments and reaffirm your commitment.

All who have accomplished great things have had a great aim, have fixed their gaze on a goal which was high, one which sometimes seemed impossible.

– Orion Swett Marden

26. Start small and commit to getting 1% better every week

When you first start exploring financial independence it’s so easy to get overwhelmed. I know I did! Following some of the stories out there, it’s hard not to go from feeling like you’re doing well to feeling like you’re so far behind. By focusing on improving everything you do by 1% every week you’ll improve your performance. See this piece on the aggregation of marginal gains for inspiration: How 1% Performance Improvements Led to Olympic Gold.

Small consistent gains can make a remarkable difference. Sweeping change can be overwhelming and making slow and steady improvements is a much more realistic path to success.

27. Keep learning

Join our email list for a regular dose of inspiration.

Check out these books:

Join an online community or Facebook group to surround yourself with people aligned with your goals

Download a podcast:

Try out an online calculator

If you want to live like most people can’t, you have to be willing to do what most people won’t. The journey won’t be easy, but it’s so worth it. Join me on my journey by signing up for my email list for continued tips, advice and motivation. We can do this together.

It must be borne in mind that the tragedy of life doesn’t lie in not reaching your goal. The tragedy lies in having no goals to reach.

– Benjamin E. Mays

Leave a Reply